ARC TDD Meeting Raises Questions About Board Vacancy, Remaining Debt, and Public Records Access

The Arnold Retail Corridor Transportation Development District met this week with three directors present: Bill Lehmann, Vice Chairman and Assistant Secretary; Dan Kroupa, Treasurer; and William Moritz, Secretary and Assistant Treasurer.

Early in the meeting, officials noted that Gary Plunk, who previously served as Chairman, has resigned from his position, creating a vacancy tied to the unusual structure of the ARC TDD board.

Board Vacancy Tied to Triangle TDD

According to the explanation given at the meeting, the ARC TDD was formed in 2008 by two local transportation authorities: the City of Arnold and the Triangle TDD. Because of that structure, the ARC TDD board includes representatives connected to those forming entities.

Officials explained that Plunk’s position on the ARC TDD board came through his role with the Triangle TDD, meaning the vacancy cannot simply be filled by the ARC TDD board itself.

Instead, the Triangle TDD will need to appoint or designate someone to fill the position. The Triangle TDD reportedly meets annually in August, though it was discussed that the board could potentially meet sooner to address the vacancy.

The discussion highlighted a broader issue for residents trying to understand who controls the district, how vacancies are filled, and where authority rests between the overlapping development districts.

Remaining Debt and Continued Sales Tax Collections

During the meeting, the board also addressed the continued existence of the ARC TDD and its sales tax collections. A question was raised about why the district would continue collecting if its own bonds had been paid off.

Officials responded that while the ARC TDD bonds have reportedly been paid, there are still outstanding obligations connected to two TIFs within the district’s boundaries. According to the explanation given at the meeting, one set of bonds is expected to be paid off in 2027 and another in 2028, unless paid off early.

The explanation given was that a portion of the TDD sales tax is tied to those TIF-related obligations through an intergovernmental or contractual arrangement. Officials said state law does not allow the TDD to dissolve while outstanding obligations remain.

That answer is likely to be one of the most important takeaways for residents following the Arnold TDD issue. The meeting made clear that even if the original ARC TDD bonds are no longer outstanding, the district’s sales tax may continue because of related obligations tied to the TIFs.

Original Project List Still Matters

The meeting also touched on what projects the ARC TDD is allowed to fund. In response to a question, officials said projects listed in the original court-approved petition remain the controlling framework.

When asked whether new projects could be added, the answer given was that new projects would require going back to court. Officials also stated that eight projects were originally listed, and that three remain incomplete.

Public Records Requests Must Go Through Board Members

Public records access was another key issue raised by citizens.

A question was asked about whether the City Clerk was the keeper of ARC TDD records or whether those records were held by the TDD’s law firm. The response given was that requests for TDD records should go to a member of the ARC TDD board, who would then request the documents from the district’s attorneys.

The attorneys present at the meeting were Debbie Rush and Mack Miner of Thompson Coburn LLP, the firm currently representing the ARC TDD.

During the discussion, it was noted that the previous law firm had represented the district for many years before representation changed around two years ago. Officials said they believe the current legal counsel has the district’s files.

However, they also made clear that citizens should not contact the law firm directly for records. Instead, residents seeking TDD records should contact an ARC TDD board member, who can authorize the law firm to produce the documents.

That process matters because many residents have been trying to better understand the original formation documents, project lists, boundaries, obligations, and financial arrangements involving Arnold’s development districts.

Separate Bookkeeping Firm Discussed

The board also discussed the possibility of using a separate firm for bookkeeping services. Officials said the district’s sales tax currently flows through a bank account and then to the trustee, U.S. Bank, which satisfies bond conditions and handles related disbursements.

A separate bookkeeping firm was discussed as a possible response to concerns raised during the state audit process.

Questions Remain for Residents

The meeting also included questions from residents about the relationship between the ARC TDD, the Triangle TDD, and other nearby districts. Officials explained that the Triangle TDD has a role in the ARC TDD because of the way the ARC TDD was formed, but other districts in the area may not have the same representative role because they were formed differently.

For residents, the meeting underscored how complicated these districts can become over time. The resignation of one board member raised questions not only about succession, but also about which entity has the power to appoint a replacement. Questions about the ongoing sales tax led back to TIF obligations expected to continue until 2028. Questions about records led residents to a process that runs through ARC TDD board members and the district’s law firm.

The meeting did not end the public debate over Arnold’s development districts, but it did provide several important answers for citizens trying to follow the money, understand the board structure, and determine where to send public records requests.

Editor’s Note

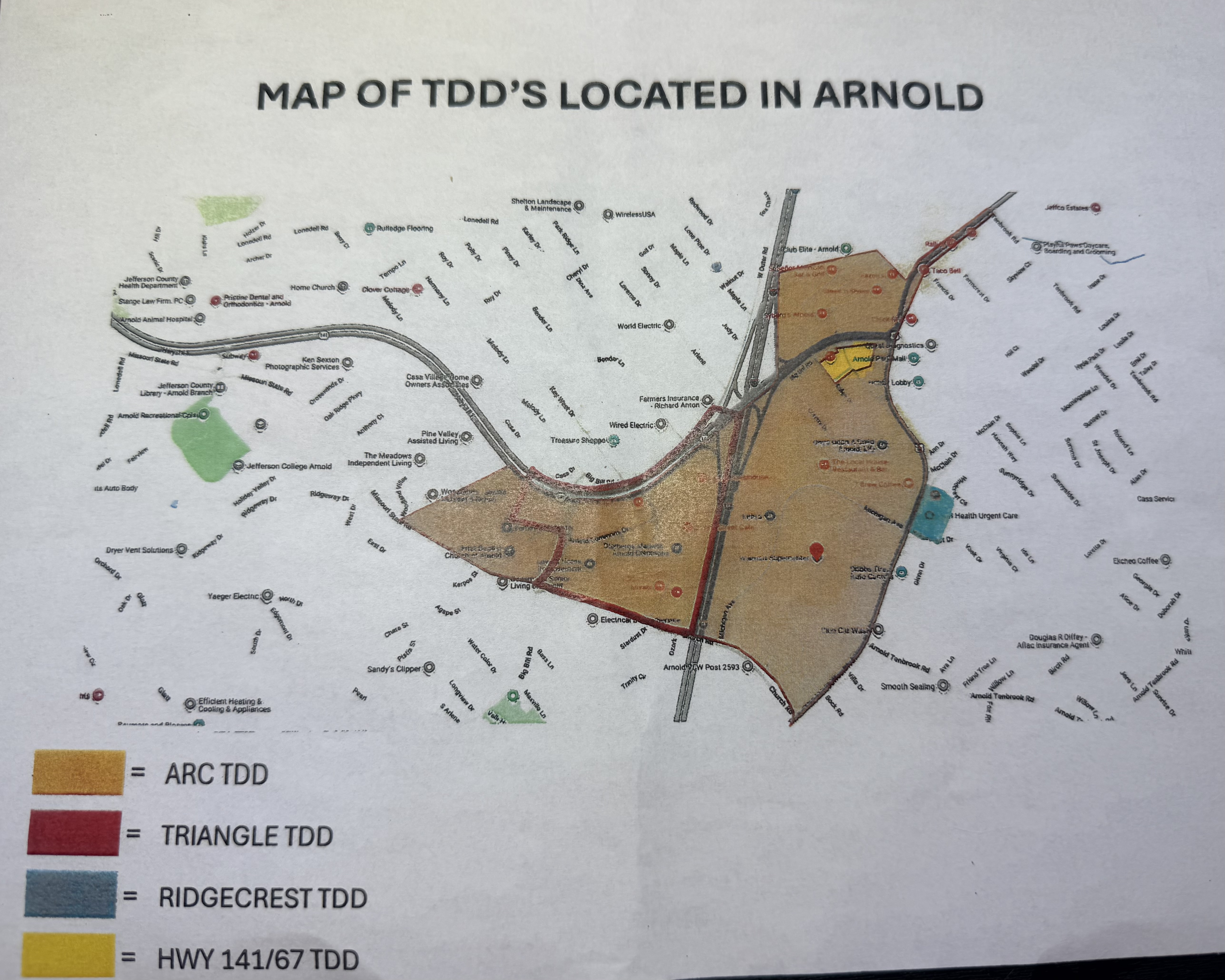

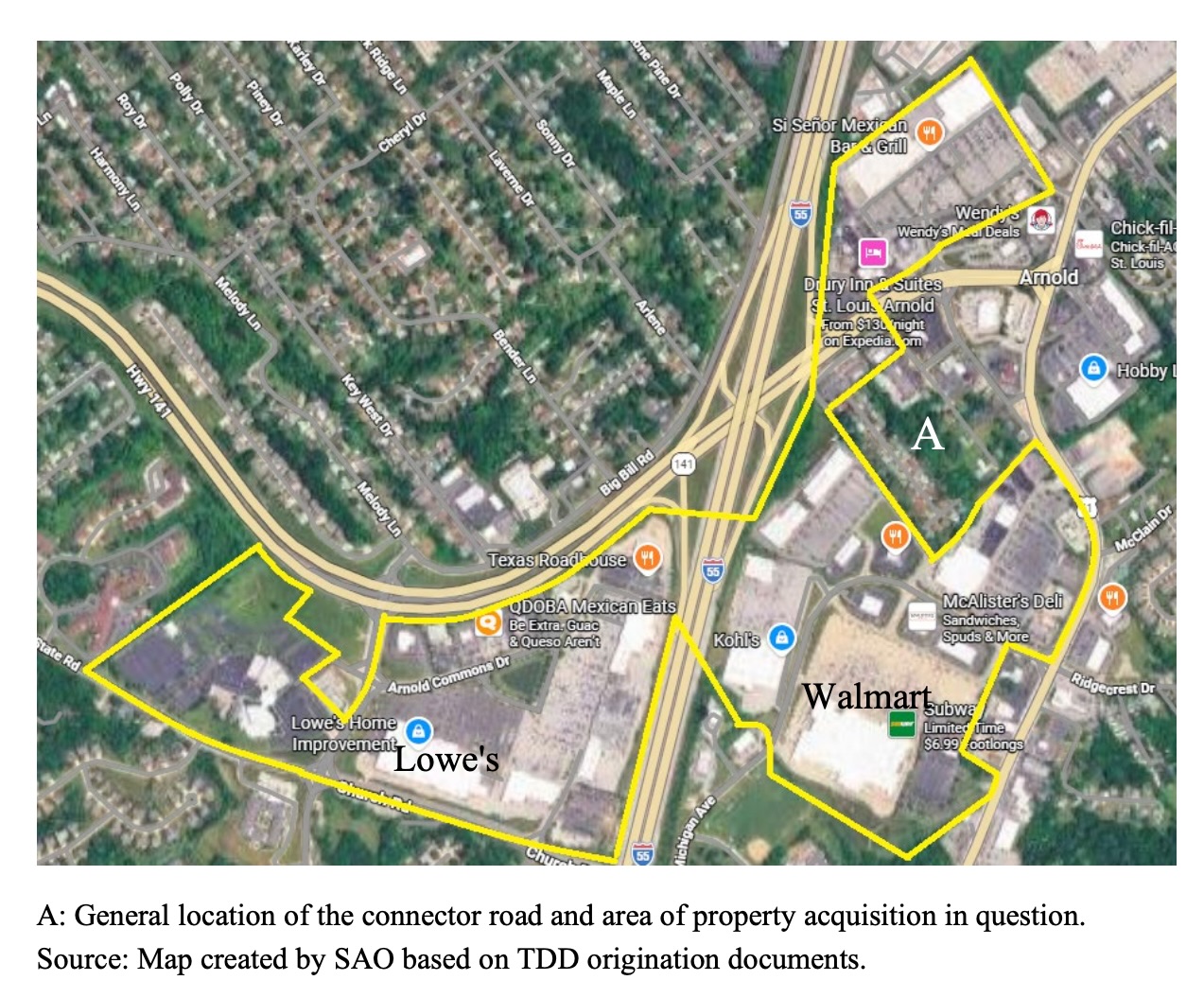

The map provided to citizens at the ARC TDD meeting appeared to differ from the map included in the Missouri State Auditor’s report. A contact from the City of Arnold told The Jefferson Review that the map provided to citizens at the ARC TDD meeting was taken from the Missouri Department of Revenue’s sales and use tax lookup website, which allows users to enter an address and view applicable tax rates and district boundaries. The Jefferson Review is noting the difference because district boundaries, overlapping districts, and which properties are included have been central questions for residents following the issue.

Stay Informed. Follow the Questions. Know What’s Happening in Jefferson County.

The Jefferson Review is committed to helping residents understand the local decisions, public meetings, and taxpayer-funded districts that shape our communities.

Subscribe today to receive local reporting, government meeting coverage, community stories, and Jefferson County updates delivered straight to your inbox.